Private credit and syndicated leveraged loans are distinct financial arrangements. Understanding the difference between the two is key for prudent investors and borrowers alike.

| Private Credit | Syndicated Leveraged Loans | |

| Privately Originated | Often | Rarely |

| Privately Negotiated | Often | Rarely |

| Floating Rate | Often | Often |

| Senior Secured | Often | Often |

| Financial Maintenance Covenants | Often | Rarely |

| Restrictions on Capital Structure | Often | Rarely |

| Call Protection | Sometimes | Sometimes |

| Control During Workout Process | Often | Rarely |

Private credit loans are directly negotiated between a borrower and a lender. This approach allows the lender to tailor the loan to fit the specific needs and risks of the borrower. In contrast, an underwriter structures terms for syndicated loans it believes can attractive enough investors to fill the financing structure.

Private credit loans typically have one or a select few lenders. A syndicated loan may have up to 200 lenders in a single transaction and involves risk that the underwriters will not be able to successfully sell the loan to lenders. Private credit also offers confidentiality for borrowers who see value in limiting public access to data.

Private credit loans rarely involve credit ratings from agencies such as Moody’s or S&P . Instead, the lender conducts its own due diligence on the company’s finances. Accordingly, private credit transactions tend to include financial covenants that are designed to protect the lender by ensuring the borrower remains financially healthy to repay the debt (e.g., maximum leverage ratio, minimum interest coverage ratio).

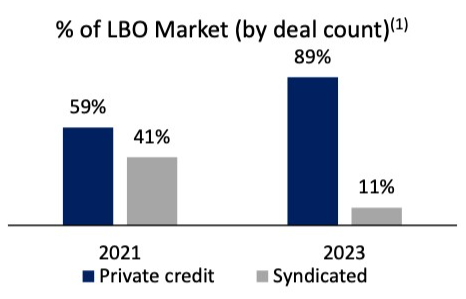

Due to the tailored nature of private credit, these loans can have faster underwriting and closing timelines compared to broadly syndicated loans. Additionally, private credit typically offers a higher certainty of size, pricing, and close. Sentiment began shifting in

2022 in the debt capital markets amid inflation, interest rate hikes, recession fears, and geopolitical uncertainty. Consequently, market share has shifted further towards private credit as borrowers place a high emphasis on certainty in volatile times. Amid an unprecedented market backdrop, we believe private credit continues to offer a greater degree of structural protection than alternative fixed income strategies and is a critical component in an investor’s portfolio.

Disclosures

Past Performance is not indicative of future results

Prospect Capital Management L.P. (“Prospect”)

Prospect is an SEC registered investment adviser that was founded in 1988 (along with its predecessors). Prospect invests across the United States in diversified portfolios by industry, company, and situation, and its proprietary underwriting process and metrics have been developed over more than 30 years and through multiple economic cycles. Prospect has over 100 employees and $11.7 billion** of assets under management as of June 30, 2023. With a buy-and-hold mentality, Prospect’s objectives are to preserve capital by making credit and equity-focused investments at reasonable multiples of recurring cash flow, earn attractive current cash yields and long-term capital appreciation while achieving consistent low-volatility returns. For more information, call 212.448.0702 or visit www.prospectcap.com

**The $11.7 billion of Assets Under Management (“AUM”) refers to the assets managed by Prospect and its affiliated registered investment advisors. AUM equals the sum of: (i) the gross assets of Prospect Capital Corporation (“PSEC”), Priority Income Fund, Inc. (“PRIS”), and Prospect Floating Rate and Alternative Income Fund, Inc. (“PFLOAT”), (ii) any amounts available to be borrowed under certain credit facilities of the investment companies, (iii) total managed assets for real estate and structured credit investments, and (iv) uncalled capital commitments. Prospect’s AUM measure includes assets under management for which Prospect charges either nominal or zero fees. Prospect’s definition of AUM is not based on any definition of assets under management contained in any management agreements of the investment companies Prospect manages. Given the differences in the investment strategies and structures among other investment advisors, Prospect’s calculation of AUM may differ from the calculations employed by other investment managers and, as a result, this measure may not be directly comparable to similar measures presented by other investment managers. Prospect’s calculation also differs from the manner in which Prospect and its affiliates registered with the SEC report “Regulatory Assets Under Management” ($8.8 billion) on Form ADV.

This information is educational in nature and does not constitute an offer to sell or the solicitation of an offer to buy any securities. Recipients should not view the past performance of middle-market loans as being indicative of future results. Prospect is not adopting, making a recommendation for or endorsing any investment strategy or particular security. All opinions are subject to change without notice, and you should always obtain current information and perform due diligence before participating in any investment. All investing is subject to risk, including the possible loss of principal. Prospect cannot guarantee that the information herein is accurate, complete or timely. We make no representation or warranty in respect of any information derived from the third-party sources which has not been independently verified.