Private credit (direct lending) has increasingly captured a larger share of the loan market in recent years, partly by refinancing borrowers from the broadly syndicated loan market. While the broadly syndicated loan market regained some ground in Q1 2024, private credit lenders countered by reducing pricing in Q2 to defend their position.(1)

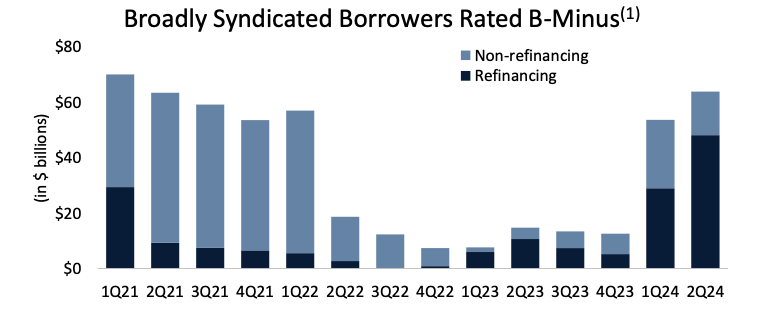

Private credit loans are typically higher priced than syndicated loans. However, the heightened competition has tightened this pricing gap, leading to a convergence in spreads. There are mitigating factors. We believe a key driver behind the recent refinancing activity is the return of lower-rated B-minus borrowers to the syndicated loan market. Data reveals that these B-minus borrowers are refinancing through broadly syndicated loans at the highest levels in years. This suggests the influx of borrowers into the syndicated market is not necessarily due to their credit quality but rather their ability to tap into a more accommodating market.

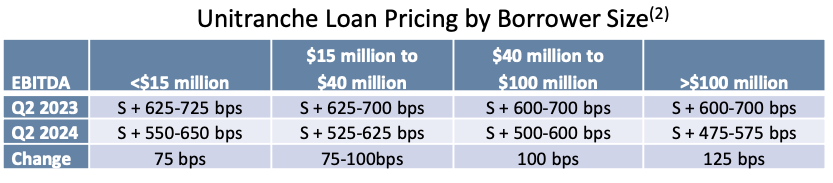

Additionally, investors may sidestep the competitive refinancing pressure by targeting the lower middle market. Unitranche spreads for borrowers with below $15 million EBITDA tightened by only 75 basis points year-over-year in Q2 2024, compared to 100-125 basis points for those with over $40 million EBITDA. We believe the difference is partially because the broadly syndicated market is typically inaccessible to borrowers with under $50 million EBITDA.

Lenders to smaller companies face less refinancing pressure, especially considering the relatively higher costs associated with refinancing. Moreover, the lower middle market typically offers lenders more favorable covenant packages and tighter legal documentation which can further mitigate risk.

Footnotes:

(1) PitchBook LCD

(2) Lincoln International

Disclosures

Past Performance is not indicative of future results

Prospect Capital Management L.P. (“Prospect”)

Prospect is an SEC registered investment adviser that was founded in 1988 (along with its predecessors). Prospect invests across the United States in diversified portfolios by industry, company, and situation, and its proprietary underwriting process and metrics have been developed over more than 30 years and through multiple economic cycles. Prospect has over 100 employees and $11.7 billion** of assets under management as of June 30, 2023. With a buy-and-hold mentality, Prospect’s objectives are to preserve capital by making credit and equity-focused investments at reasonable multiples of recurring cash flow, earn attractive current cash yields and long-term capital appreciation while achieving consistent low-volatility returns. For more information, call 212.448.0702 or visit prospectcap.com

**The $11.7 billion of Assets Under Management (“AUM”) refers to the assets managed by Prospect and its affiliated registered investment advisors. AUM equals the sum of: (i) the gross assets of Prospect Capital Corporation (“PSEC”), Priority Income Fund, Inc. (“PRIS”), and Prospect Floating Rate and Alternative Income Fund, Inc. (“PFLOAT”), (ii) any amounts available to be borrowed under certain credit facilities of the investment companies, (iii) total managed assets for real estate and structured credit investments, and (iv) uncalled capital commitments. Prospect’s AUM measure includes assets under management for which Prospect charges either nominal or zero fees. Prospect’s definition of AUM is not based on any definition of assets under management contained in any management agreements of the investment companies Prospect manages. Given the differences in the investment strategies and structures among other investment advisors, Prospect’s calculation of AUM may differ from the calculations employed by other investment managers and, as a result, this measure may not be directly comparable to similar measures presented by other investment managers. Prospect’s calculation also differs from the manner in which Prospect and its affiliates registered with the SEC report “Regulatory Assets Under Management” ($8.8 billion) on Form ADV.

This information is educational in nature and does not constitute an offer to sell or the solicitation of an offer to buy any securities. Recipients should not view the past performance of middle-market loans as being indicative of future results. Prospect is not adopting, making a recommendation for or endorsing any investment strategy or particular security. All opinions are subject to change without notice, and you should always obtain current information and perform due diligence before participating in any investment. All investing is subject to risk, including the possible loss of principal. Prospect cannot guarantee that the information herein is accurate, complete or timely. We make no representation or warranty in respect of any information derived from the third-party sources which has not been independently verified.